Πηγή: Wolf Street

By Wolf Richter

Aug 14 2014

“The glue of the sanctions is starting to dry,” mused Sergio Trigo Paz, head of emerging market fixed income at BlackRock, the world’s largest asset manager. Investors fret that holders of Russian corporate bonds might not receive interest payments because a “blocked person” has a large stake in the company, he said. “All transactions could start to freeze.”

That was in mid-May. Now, the glue has dried: Igor Sechin, CEO of Russian oil company Rosneft and a major shareholder, whose name graces the “Specially Designated Nationals and Blocked Persons List,” is begging the Russian government for a $41.6 billion bailout in response to the sanctions.

The company has net debt of $44.5 billion, the hangover from its $54 billion acquisition of TNK-BP last year. But the US sanctions ban loans to Rosneft with maturities over 90 days, and EU countries are sticking to these sanctions as well. So dealing with this debt and paying dividends is going to be tough.

And the advance payments from China from the Holy-Grail gas deal that analysts had seen washing over Rosneft? $63 billion between 2014 and 2018, according to Raiffeisenbank’s energy specialist in Moscow, Andrey Polishchuk, who didn’t think Rosneft would have any problems paying its debts and dividends “until 2019.” A hype-ventilating analyst’s pipedream for now.

But Russia’s National Wealth Fund, where the bailout money is supposed to come from, already doled out much of its $86 billion for other projects and cannot fund the bailout, according to the Vedomosti newspaper (picked up by Reuters). The paper cited government sources and a letter from Prime Minister Dmitry Medvedev that asked officials to analyze the request, which one of the unnamed officials called “horrible.”

Thus, the sanctions are beginning to wreak havoc. Everywhere. German industrialists and exporters have long complained about them. CEOs step up to the microphone on a near daily basis and, after pronouncing the requisite pledge to submit to the “primacy of politics,” slam the sanctions and the impact they have on their companies. They’ve been doing this for months, trying to jawbone the German government into compliance with their needs.

Now the official results are in. And they’re ugly.

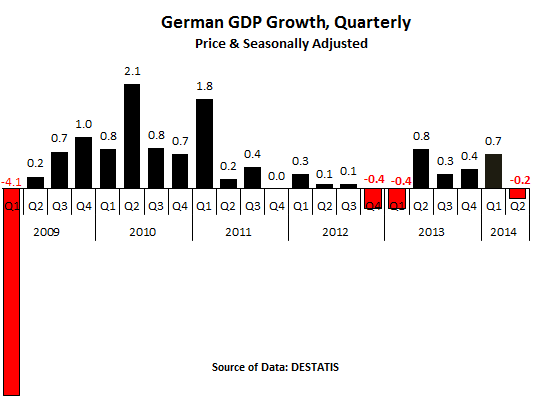

Germany’s economy shrank 0.2% in the second quarter from the first quarter, worse than feared recently, and much worse than the blue-sky forecasts from earlier this year. As the chart shows, the economy has been languishing for three years – with the exception of two quarters – in low-growth purgatory, interrupted by a technical recession of two consecutive negative quarters.

The German statistical agency Destatis blamed exports; or as it said, that imports outpaced exports, thus bringing down the trade surplus. The German economy can’t do without a big trade surplus. It lives and dies by it. But it didn’t blame exports to Russia specifically, which would have been too politically charged. Russia ranks in 13th place on the list of German export destinations, but it’s still important, and exports have swooned [Sanction Spiral Successful: German Exports to Russia Plunge].

The data in Q2 preceded the tragedy of Malaysian Flight MH17 and the subsequent tightening of the sanction spiral and Russia’s countersanctions. Companies on both sides are now beginning to feel serious heat. Unless a miracle happens, Q3 is going to be tough.

Destatis also blamed the weather, of course. Investments in construction declined, after the balmy winter weather in Q1 had apparently caused builders to frontload their activities. Private and public consumption however were up, for which the weather wasnot blamed. Compared to a year ago, real GDP edged up a measly 0.8%.

Germany, the vibrant economy, the big locomotive of the Eurozone, didn’t just stall. It reversed direction. And it dragged what little growth there was in the 18-member Eurozone into stagnation. France, the second largest economy, had no growth – for the second quarter in a row! Italy declined 0.2%. And GDP for the Eurozone remains 2.4% below its pre-financial crisis peak. This is the picture of the “recovery” in the Eurozone, though no one has yet told the stock markets which have been soaring for years. And hope is already spreading that the recent hiccups won’t be anything but blips on the way up into the stratosphere.

But each country has its own set of problems. In Italy, which is now in a perma-recession, the government refuses to pay its suppliers. It’s a way to keep its fiscal disorder under wraps and bamboozle the markets, but it’s strangling the private sector. Read…. Italy’s Economic ‘Recovery’ from Hell in One Chart

No comments:

Post a Comment